Keep up with the latest FinTech and private market news, business tips, and thought leadership from industry leaders, mentors, and professionals.

Join our mailing list to receive information on upcoming Helicap platform updates and webinars.

If you're excited about the potential of private markets and fintech, we've got a job for you.

Helicap recently hosted a fireside conversation between David Z. Wang, Co-Founder and CEO of Helicap Securities, and Jeffrey Jaensubhakij, Advisor and former Group Chief Investment Officer at GIC, Singapore’s sovereign wealth fund. With nearly three decades of experience at GIC, Jeffrey oversaw capital allocation across asset classes, regions, and investment mandates, giving him a rare vantage point on capital allocation, risk management, and long-term investing across multiple cycles. The conversation covered macroeconomic policies, geopolitics, artificial intelligence, private credit, and the discipline required to navigate changing market conditions. It was a candid and thoughtful exchange amongst the investors and partners who joined us.

We hope the reflections below offer insights into the key themes discussed.

Our evening's speaker needed little introduction. Dr Jeffrey Jaensubhakij brings decades of experience at the highest levels of institutional investing, having spent his career at GIC, Singapore's sovereign wealth fund. Most recently serving as Group Chief Investment Officer, he oversaw capital allocation across asset classes, regions, and both internal and external investment mandates — a role that placed him at the centre of some of the world's most consequential investment decisions. Over the course of his tenure, Dr Jaensubhakij led GIC's Public Markets Investments team and headed its European Operations, Global Equities, and North American Equities teams. Today, he continues to contribute to the investment community as Advisor to GIC, trustee of Singapore Management University, Chair of its Investment Committee, and member of the Advisory Board of the Sim Kee Boon Institute of Financial Economics.

He holds a Bachelor of Arts in Economics from Cambridge University, and a Master's and PhD in Economics from Stanford University.

The evening began with a lighter segment: ten unscripted rapid-fire questions. Jeffrey’s responses were refreshingly direct and helped set an open, thoughtful tone for the discussion that followed.

The conversation moved into Jeffrey’s career across multiple market cycles. When asked which crises had tested or surprised him the most, his answer was less about the crises themselves and more about the policy responses that followed. Jeffrey shared that he had been somewhat bearish throughout his career, often sensing that market booms contained weaknesses that could eventually surface. The Thai Baht crisis, NASDAQ bubble, and U.S. mortgage crisis did not, in hindsight, feel particularly surprising to him. What did surprise him was how quickly central banks and fiscal authorities responded each time, flooding markets with liquidity and support. But here is what shaped his thinking about markets today: "Each time the Fed supports something, it creates an environment of complacency that allows a bubble or excess leverage to build somewhere else, not in the same place as before."

This observation framed a broader discussion on where excess leverage may be building today, whether in AI, private credit, or elsewhere in the market.

One of the broader themes that ran through the evening was the delayed impact of policy. Jeffrey drew a distinction between the immediate market reaction to policy announcements and the deeper adjustments that follow as companies, governments, and investors adapt. His example was US-China trade tensions. What mattered most was not the tariff announcements themselves, but what followed: a structural reorganisation of supply chains, with companies moving operations into Vietnam, Indonesia, Southeast Asia, and Mexico. For investors able to participate through private markets, he noted, it has been a durable and underappreciated opportunity with a long tail still playing out.

The same logic applies more broadly to the current U.S. policy environment. When a policy becomes less predictable, for adversaries and allies alike, the natural response is likely a gradual diversification away from dollar assets and dollar-denominated trade. Jeffrey noted this shift may not be visible in near-term data, but over two to three years, it could become meaningful, showing up in currency flows, regional payment systems, and Europe’s efforts toward greater financial autonomy.

The conversation then turned to the Iran conflict, where Jeffrey’s view was that the disruption extends well beyond oil. Chemicals, fertilizers, sulfuric acid, helium: two months of inventory drawdown across these inputs represents supply that, in his view, will not be recovered. He expects the economic impact to show up with a lag over the next six months, with Asia particularly exposed as a primary end-market for many of these commodities.

The discussion moved to interest rates, where Jeffrey offered a more nuanced view of how central bank policy could evolve from here. His view on Fed leadership was thoughtful and measured. Kevin Warsh, historically known as a “hawk” who questioned quantitative easing, appears to be laying groundwork for potential rate cuts by pointing to AI-driven productivity gains that could help contain inflation. Jeffrey noted that Warsh may not have the full Federal Open Market Committee (FOMC) in agreement, but expects him to push the case for cuts. If the economy does not accelerate from here, Jeffrey suggested Warsh could make that argument sometime this year, and one or two cuts would not be surprising. But he also pointed to a meaningful constraint worth considering: "The Fed can cut rates and fiscal policy can support markets until inflation gets so high that they lose all credibility if they keep cutting."

The question is how these two forces balance out: Will AI productivity gains suppress inflation as some anticipate? Or will higher energy and agricultural costs from supply disruptions push inflation back above 3-3.5%? Jeffrey’s observation was that if governments lean on fiscal stimulus to cushion a 2027 slowdown, the resulting inflation pressure could put the Fed in a position where cuts reverse into hikes, a scenario he does not see as out of the question. He gave an example to illustrate the challenge: fuel subsidies being implemented in some Southeast Asian countries right now. When there is an oil supply shortage, subsidizing consumers to buy fuel does not create more supply. It maintains artificially high demand and can push prices higher. Well-intentioned policy, but potentially inflationary in its effects.

The conversation then shifted from macro policy to technology, with AI becoming one of the evening’s most layered discussions. Before diving into the investment question, David shared a personal observation. One afternoon, he asked his kid what he was working on. The answer: Japanese homework, using Gemini. His teachers have essentially accepted that students will use AI and are now adapting how they assess learning. It was a small but telling glimpse of how quickly this technology has become part of everyday life. Given GIC’s investment in Anthropic, David asked Jeffrey for his perspective on AI broadly, and specifically about healthcare applications.

While Jeffrey remained cautious about the broader economics of AI, he was more positive about sectors where the benefits are clearer, particularly in healthcare. Aging populations will demand more care that becomes increasingly difficult for governments to subsidize, creating a substantial cost problem that needs addressing. The question is whether AI can tackle it effectively. Jeffrey explained: "We don't, as a society, whether Singapore or the U.S. or elsewhere, actually go through medical records, do comparisons, try to figure out what are the behaviors, the precursors of disease that you can actually spot, which you can do preventative treatment for." AI can analyze this data at scale, and the economics make sense. Preventative interventions, even with upfront costs, can save considerably by reducing expensive late-stage treatments. Healthcare also has a unique advantage: vast datasets across millions of patient records, all within the analyzable parameters of human health. Jeffrey sees healthcare and finance as two sectors with profit pools potentially large enough to justify the AI investment, and areas where meaningful progress is already visible.

The broader AI discussion was more cautious. Jeffrey acknowledged that demand appears enormous, but posed the investor question: how much of that usage is actually monetised? Much of it remains free or subsidised, and the economics behind the headline numbers tell a more complex story. Revenue growth has been strong, but costs have grown faster, and the leading AI companies are not projected to break even until around 2030.

He drew a parallel to the dot-com era, where real revenues and real infrastructure masked the fact that underlying business models depended on continued financing rather than profitability. The fundamental question, in his view, is whether these companies achieve profitability before the funding environment shifts.

David raised a counterpoint: some of today's most valuable companies, including Amazon and Facebook, spent years prioritising growth over profit. Jeffrey acknowledged the parallel, but noted that in each case, the turning point came when management found a credible path to monetisation. His view is that adaptive leadership, teams that are constantly looking for additional ways to generate profit, is ultimately what separates the companies that endure from those that do not.

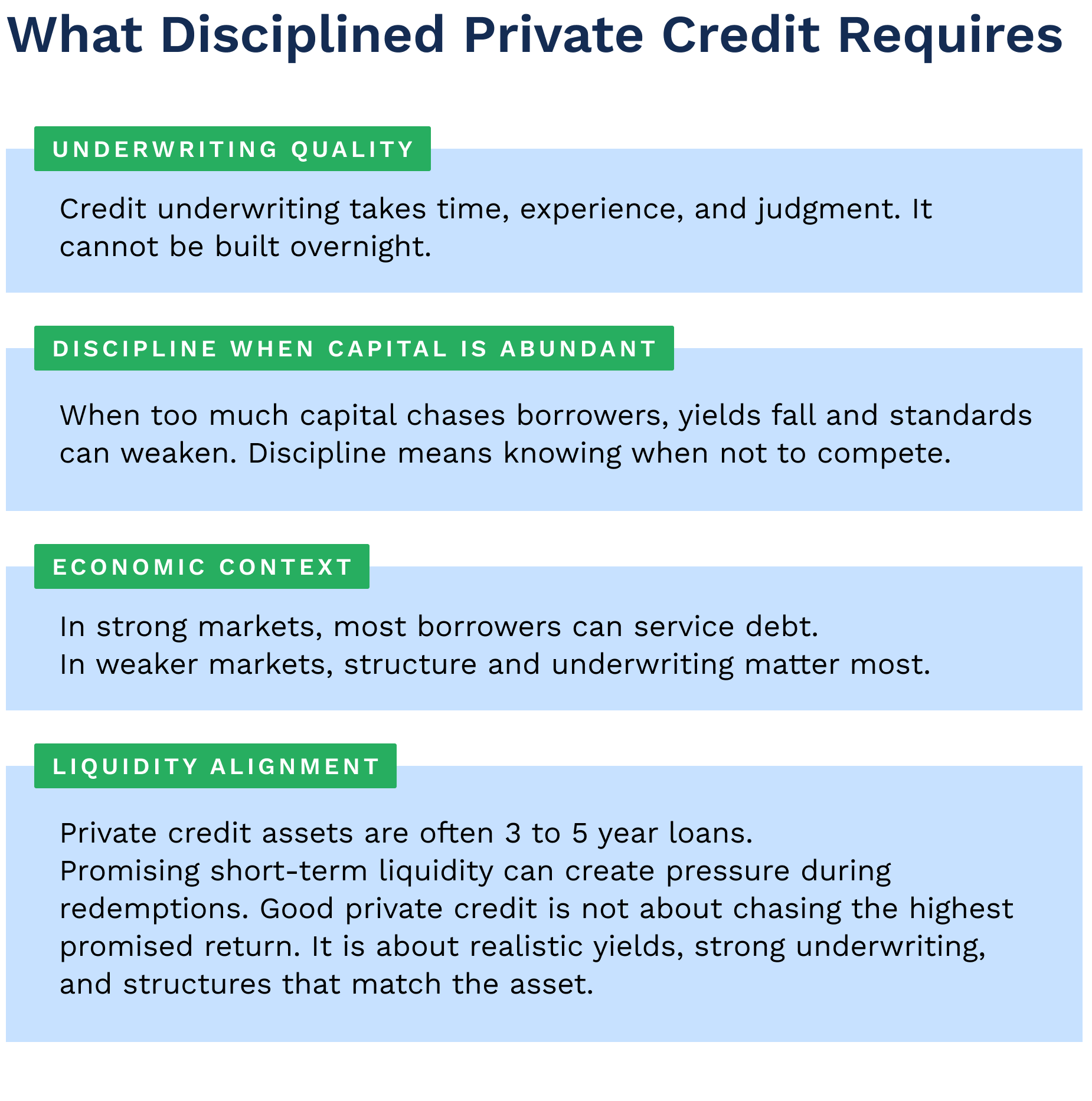

The conversation then moved to the topic that first connected David and Jeffrey three or four years ago: private credit. David noted how the asset class has grown rapidly in prominence, with the market now around $2 trillion and projected to reach $3.4 trillion by 2030, alongside increasing attention on redemptions, valuations, and credit structuring. Jeffrey congratulated Helicap on its 8-year track record and discipline before sharing his observations on what matters most in credit investing:

Later in the conversation, Jeffrey referred to private credit as an example of a more realistic return profile.

In his view, a strong manager with sound underwriting can offer returns in the high single digits today. Even after accounting for losses, well-underwritten private credit, he notes, can still deliver meaningful returns.

As the evening drew to a close, David asked Jeffrey about his plans post-GIC.

Jeffrey reflected on how challenging it is to consistently achieve good returns, noting that what looks attractive in hindsight may not be in the future . He noted that in 2011, Asian equities had delivered annual returns of about 17% returns, which led him to encourage his family to invest on that basis. However, over the following 20 years, returns were closer to 5% returns per year.

Beyond returns, he has observed how difficult it is to control emotions, even for institutional investors. Tariffs go up, markets drop, everyone else is getting rich, and behavioral patterns can often prevent investors from being as consistent as they aspire to be. He is looking to build a business that focuses on helping investors gain more certainty in returns and avoid those behavioral mistakes. He reflected that delivering consistent real returns may matter more than pursuing promised returns that ultimately fail to materialize.

It was a privilege for Helicap to host this conversation and hear Jeffrey’s candid perspectives, shaped by nearly three decades at GIC. His insights on discipline, long-term thinking, and navigating changing markets resonated with everyone in the room. We thank Jeffrey for his openness and thoughtful engagement, and we are grateful to the investors and partners who joined us.

Enjoyed this recap? We publish regular insights on private credit, emerging Asia, and the conversations shaping alternative investing. Join our mailing list to stay in the loop: Subscribe to Helicap newsletter

Disclaimer: This blog is based on Helicap’s May 7th 2026 fireside conversation with Jeffrey Jaensubhakij. All insights are drawn from the session.

Investment involves risk. Past performance is not necessarily a guide to future performance or returns. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Helicap Pte. Ltd. (“Helicap”) and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Helicap, its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider (i) whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. You may also wish to seek financial advice through a financial advisor or and independent legal, accounting, regulatory or tax advice, as appropriate.